There used to be a time when I tracked all my spendings – every month. For years. After I earned more money and didn’t need to budget this closely anymore I got a bit lazy about it. And some time in the past couple years I realized I have no freakin clue were my money goes. Well, I do somewhat as I need to set pricing for my freelance business and see if my hourly/daily price covers my spendings. So I know round about what I need to earn and I know my big spenders. However the nitty gritty in-between, the moments money seems to fly out of your wallet those are the moments I couldn’t pin point.

When I set my new list of goals for the 101 things in 1000 days I knew I wanted to include tracking my spendings. And so here is the first month I am doing it. For my October spendings 2022 I tried to lock down all my spendings. Read my spendings. Not household spendings. That would be a goal for next year.

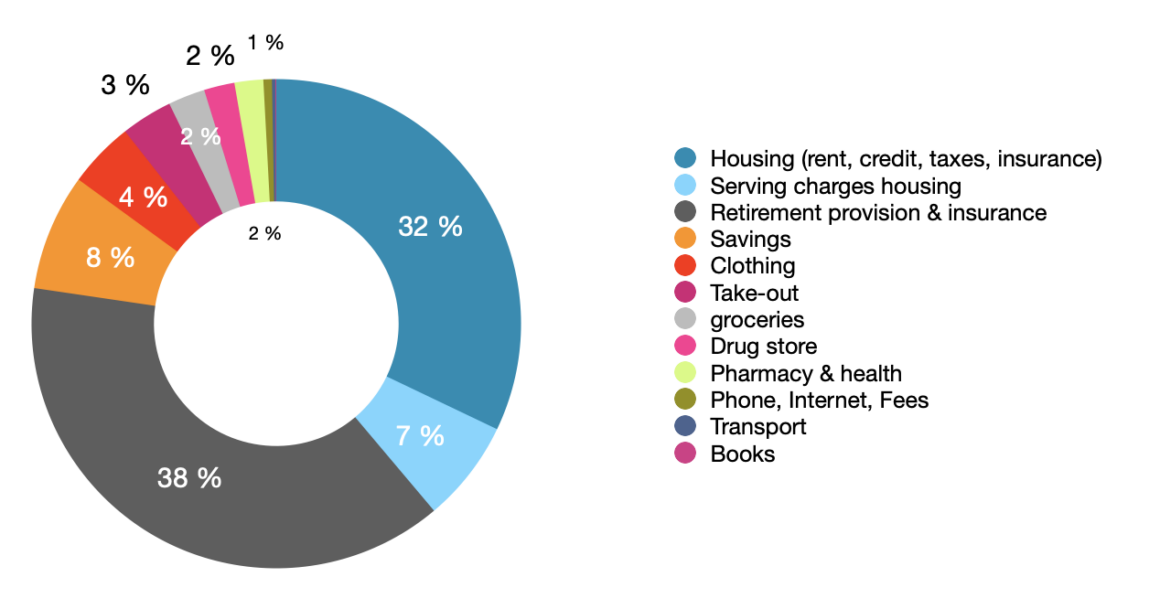

When you look at this chart you see that I pay about as much for insurances and retirement (38%) then for housing (32% +7%). Now please keep in mind housing is only the share I pay. It is double the money.

Insurance spendings

But paying this much for insurances is really really annoying. And it is only the monthly payments. I have insurances like my business insurance or my international health care that I pay annual and that don’t fall into October. My health insurance is high. As a freelancer I have to cover that all by myself and the more you earn the more it goes up. Currently it is close to 1,000€ a month. I want to weep when that payment is taken out of the account. But than I quickly try to tell myself that I am still better off. My migraine medication alone is 600€ per month. I had a surgery this year and all the regular appointments such as dentist, gynecologist, ophthalmologist and my regular doctor and all the vaccination. So it is a good deal. But it does hurt.

As a freelancer I also have to save up some money for my retirement. I do not have any employer taking care of that. I do have a couple insurances for that – not the best options but I was young. I also try to build up a portfolio to close the gap I am having for retiring.

Spendings for Savings and freelance life

I like to save as much as I can. Currently that is 8% a month. This is a bit fluent. If I spend less I put more in savings. Less in December as I have all the Christmas spendings. However ever since I started full time work I have tried to put some money into savings. And I know I am a rare breed when I say I have never been in dept in my life. Very privileged. Very thankful. But I know life can quickly throw a curve ball. Specially when being a freelancer. And who am I kidding hard years are to come. I don’t have any illusions about 2023 and 2024. I will most likely reduce all those savings… It is an up and down that freelance gig.

Maybe a quick side note since I dipped into freelancing. I do have two separate accounts. And I pay myself a monthly salary from my business account to my private account. That salary is fixed (at least for a year) and if I earn more I don’t get a raise. But I also don’t get cut when freelance work slows down a bit. I try to have a steady income that is oriented on my spendings.

The savings here in the diagram are additional savings as a private person.

Spendings in Clothing

I am a little surprised about that spending but then not really. I usually do not buy so many new clothes and don’t care much about fashion trends and the latest must haves. However this month I finally found a rain coat. I have been searching for years. I also needed some new underwear – 2 bras broke… I snatched a royal blue sweater on sale. I had the same one bought earlier this year but it broke (I was refunded) and missed it ever since. As it was on sale it was a no brainer. Also two shirts I had in my cart since summer. And then I invested in some warm slippers for winter. I get really cold feet when sitting in the home office and work. Cold feet are no good – for health and mood reasons. One pair would have been enough the husband said I should keep both. I did but I could have done with one…

Spendings on Food

Is it sad that I spend more on take-out than on groceries? Admittedly yes. I wished it was the other way around. It is not. And exactly the reason I needed this spending report. I needed to see it with my own eyes. I know we do a lot of take out. Laziness wins. Or it is some sort of gender equality. I don’t want to cook every day. The husband doesn’t want to cook at all and so it is take-out. Also when we are both really really busy with work we order in and keep working.

Again this is only the amount I spend on food. Often times the husbands orders groceries and take out. I assume he pays more. So not really representative I fear.

Also some of the groceries I get are bought at the drugstore. I was just too lazy to split the bills in two categories. The drugstore carries a lot of organic foods. I get my oat milk, healthy candy, cracker and nuts, honey or at times noodles or flour.

As you can see I don’t really spend anything on hobbies or myself. Books are the bottom of all with a total of 1,98€ spend – two kindle books. I didn’t buy craft supplies. This blog domain costs sure but I run that through my business as I have a website there too and my package allows for three websites in total. Should I spend more on hobbies and myself? It is something I really have a hard time with. (Hence making it a goal this year and giving me a budget even) I think I can splurge for the rest of the year…

I have not tracked the October spendings 2022 religiously. I could have done a better job but I didn’t want to spend more time on it. However it will be interesting to see what it will look a year from now.

Do you track your spendings? What is your surprise when you look at the spendings?

Happy spending

16 comments

I do track our spending each month! It takes 10 minutes and it’s nice to have a snapshot of what’s coming in and going out!

I don’t currently own a raincoat and really should invest as we get plenty of rain here in Atlantic Canada; I love your coat! Such a gorgeous colour and looks so chic on you!

Ten minutes only? Wow. I always spend so much time. Maybe I am to meticulous. But I agree knowing what comes in and goes out is a good thing to have an overview of

I do keep track of our spending but not as detailed as you. I feel like I have a pretty good grasp on it. When we bought the house we went to a financial planner to make sure we can afford it but she basically confirmed what I already calculated. It was money well spend nonetheless. It was very informative.

I dont keep a monthly budget. Way too lazy but it does help knowing. I bet the financial planner was really helpful – sometimes you just need validation from pother people and a pat on the shoulder.

I find this fascinating! We keep a monthly budget but it’s just our outgoings. I used to have to budget more because I had to make sure we had enough money – now that we’re better off I just track what we spend to keep track of where it is going. We have budgets we try to stick to and seperate it into Bills/Food/Clothes/Hobbies/Kids/House/Misc. It would be interesting to make a pie chart like yours. We also do a snapshot of our net worth every month just to make sure the overall trendline is going in the right direction (well it’s mostly flat because we pay so much for nursery right now).

Being freelance must be so hard because you see all your outgoings. My retirement comes straight from my paycheck, as does my health insurance. I think I would feel worse to write a check once a year!

Thanks for the peek into your spending :-)

I think budget in general and money is a tough thing. We don’t really get taught much. about it growing up and then suddenly we need to know it all in. an instant. I am very glad I have a commercial background but half the time I still am not sure. The budget I showed here is only private expenses the freelance ones are a whole new topic….

As you probably know, I am – and have been – tracking our spending for a long time. Like Elisabeth, it usually only takes me a few minutes here and there, filling in purchases as they come in. The initial “setup” took a little longer, but now I basically budget as I go.

I was shocked to hear that you pay 1000 Euros for health insurance. That’s a big chunk of money.

May I ask: do you and Eddy keep all your expenses separate? Or are you only “presenting” your side of the budget?

Honestly just curious, I know things work differently for everyone – some people combine everything, some people have a shared account but also “separate” ones, too. It’s fascinating to me how couples work that out.

Yes the health insurance is always a shocker. It makes me mad every time but than I run down the numbers and see it. is not soooo far off. However. I am sure I am paying more than I need in the long run. I am a bit scared in how far the fees will rise with long covid and all.

In this post I only “Present” my side. Mainly because I didn’t want to add his expenses out of laziness. And I don’t know them all. I know it is fascinatin how couples approach this. When we were first pondering the question to go forward in our relationship we had big discussions about it. Back in the day we would do monthly budgeting meetings. We would save up all bills and by the end checked if anyone had more expenses and then pay accordingly. When we got more serious, we stopped that practice. As for your question: we do have two separate accounts (currently my preference, the husband would like just one) and a shared account for housing, insurances things all things regarding US. But it is a constant thing we discuss. As we are both self employed and the husband has a company I am not sure in how far legal activities go to dip into my money when things go south. So until I know more I would like to keep it separate. Also a more practical thing I dont want him to know what I get him for presents…

Here in the US, there is a perception that in Europe, all medical expenses are ‘free’. Meaning, we know they come out o taxes, but have no idea about monthly premiums. Wow, those seem high to me…and then again, when i read that you are self employed, not high at all. In the US, it is a combination of employer and employee payments. Currently, we are on 3 different plans for 3 people in our household. There is a better way, this Is not it.

I track our bills, but other than that, I do not track our spending. Meaning, mortgage, utilities, and so on. We have separate accounts for our own money, and a joint account for bills. It is not perfect or completely equitable, but it works for us. We’ve been together for over 30 years, and have had our issues, but never about money. Not saying that works for everyone, but it works for us.

Well nothing is really free. It is “free” for everyone somewhat. You need to have health insurance and the insurance companies need to to take you even if being terminally or chronically ill. The monthly rate is paid by you (reducing your salary hence paying less taxes) and 50% your employer. Since I am freelancing I have to pay it all myself. Germany is compared to other countries not really self-employed friendly. I could switch my insurance company to a private provider making me pay less. But I would not be able to return to a government plan later on. And since I do have some chronic diseases it is overall better to stay. Its a very complicated system and I am not sure I fully understand it.

As for the accounts – that is how we do it too. And we nalso have our issues but not really over money. I hear its a bit discussion for many.

I used to track all of my spending monthly, but it was sort of exhausting, to be honest. I’m job hunting, so maybe I’ll resume when my income is a bit more stable!

I dont want to do that all the time either. Very exhausting. And I believe if you do have some sort of overview and are responsible in spending money it should nit be necessary. Goof luck job hunting.

I track my spending! It’s something I started doing a few years ago because I needed to get a better handle on where my money was going. Right now, I do quarterly spending reports but I may switch back to monthly in 2023 as I want to be better about sticking to an actual budget.

Also, hooray for someone else who gets a lot of takeout! It’s just so much easier for me most nights, lol, even though it’s so much more expensive than eating in.

It is the luxury we grant ourselves as busy people. I dole to cook occasionally but when it becomes a chore…. ughhh

Way. to go for monthly and quarterly spendings. I am too lazy but I think I need to be a bit more attentive to our outgoing money. And I am not talking about the big bills more the here and there and in between spendings.

This is so interesting to see – particularly because you don’t live in the US, and I do. The insurance took me aback when I first looked at the pie chart, but made much more sense after reading your explanation. I honestly don’t think I could ever freelance or be self-employed… the lack of a guaranteed minimum monthly amount would likely drive me bonkers!

My food costs are the opposite of yours – probably 95% of my meals are eaten at home, with take out/restaurant meals occurring far less frequently. Then again, I am a hermit, and like to eat what I like to eat… so… :)

It definitely is a bit of a rollercoaster to be a freelancer but it is the life that works for me. Maybe that changes in the future who knows. I would love to eat more self cooked meals but I am often so lazy at the end of the day. I know some people see cooking as a sort of self care and relaxation. Not me. It is more a chore.